Rate Hawk Down

By Benjamin Picton, elder macro strategist at Rabobank

Bonds sold off on Friday and the NASDAQ closed a smidgen lower. Both the S&P500 and the Dow Jones managed insignificant gain, with the Dow’s outperformance against suggesting that equities proceed to trade on sensitivity to discount rates. Two-year years rose 3bps on Friday while 10-year years managed a gain of 4.7bps, bear-steering the curve.

Brent crude is trading just a contact above Friday's close of $83.98/bbl, despite news over the weekend that the Iranian president Ebrahim Raisi is missing after a chopper carrying both he and abroad Minister Amirabdollahian cracked in mountainous land in the country's north-west. Last reports propose that the wreckage has been spotted by search teams, but that no signs of life have yet been detected.

While there is no proposition of foul play, it is absolutely not perfect for elder Iranian political figures to be active in chopper contributors while pressures between Israel and Iran stay in a heightened state. The Economist has suggested that if Raisi has been killed it could set off a power conflict in Iran as he was a leading candidate to become the eventual success for ultimate Leader Khameini. Nevertheless, the reaction in the energy complex suggestions that traders reconstruct untroubled by the news.

Shifting is an interesting rate world, The post-CPI jubilation had clearly begun to wane at the end of last week as a number of Fed speakers took turns watering down the proven punch bowl. Mester, Williams and Barkin all talked down the prospects for rate cuts, suggesting that possible, maybe, it might be appropriate to cut rates before the end of the year. Or it might not.

Mester – 1 of the FOMC’s more hawkish members – will be stepping down at the end of June. She scores +1 on Bloomberg Economics’ hawk/dove spectrometer. Under the FOMC’s current composition, the Spectrometer sums to zero (neither hawkish nor dowish), which means that the inviting president of the Cleveland Fed – who will regain a vote associate in 2024 and 2025 –has the possible to tip the Fed’s overall bias in either direction.

Meanwhile, Bowman (perhaps the FOMCs bridge hawkish member) said that advancement on Labour marketplace re-balancing has slowed, the Fed is monitoring to see if policy is efficiently revived, and she is willing to hike again if inf inflation springs.

We could carry Fed speakers for coaching Tentative predictions of future rate cuts in caveats around the possible for inflation to emergence again. Last week’s CPI – while welcome – was the first release in 3 months that didn’t surprise to the upside. After the Powell pivot summertime last year sparked frenzied specification of the timing and quantum of rate cuts, it only sees intent to be a small more circumspect this time around erstwhile the data falls the Fed’s way.

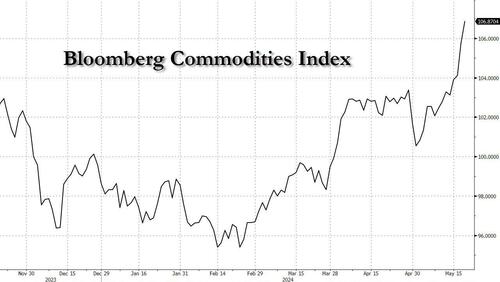

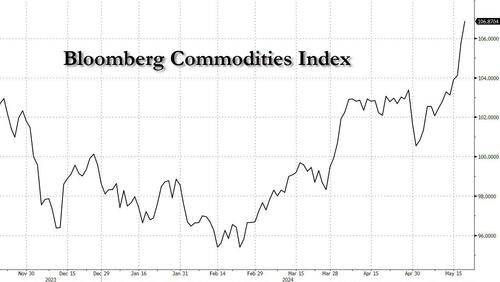

Indeed, The Bloomberg communities index is informing not to compose inflation’s obituary just yet. It has been ralying since February and is now at its highest reading since October last year. Cocoa has pulled back permanently since its April highs, as have cotton, sugar and coffee, but these have been more than offset by fresh runs in aluminum, nickel, copper, silver, iron ore, steel, orange juice concentrated, soybeans, Wheat, beef, gold, natural gas and diesel, while the fresh ban on integrated uranium imports from Russia could besides add to price pressures in the atomic fuel supply supply chain. Higher community prices are familiarly unhelpful while core services inflation restores a problem.

Overall, It seems that we’re back to “waiting for more data” for the time being, but the May FOMC gathering minutes due out later this week will inactive be a key point of interest for markets.

The Reserve Bank of fresh Zealand will be another point of interest as it meets to set the authoritative cash rate. No changes are expected from the prevailing 5.50%, but the scheduled release of the Monetary Policy message – which includes updated forecasts – will be crucial for the local market.

The RBNZ has established a reputation as something of a bellweather for global interest rate cycles. With the economy in recession and the labour marketplace showing fresh signs of fast softening, it will be worth keeping an eye on how the RCNZ flags the ability of an earlier cut to the policy rate than their current mid-2025 guide.

The minutes of the RBA's May policy gathering are besides due to be released this week and may supply a point of contrast. While the RBNZ has the luxury of a single focus on inflation, the RBA must reconcile its price stableness nonsubjective with a full-employment mandate. That testbly goes any way toward exploring the absence of any hawkish tilt from the RBA in May, even as Q1 inflation and Labour marketplace data prior to the gathering had been amazing on the strong side.

As Leonard Nimoy erstwhile said “If you pursuit 2 rabbits, you will lose them bothIt’s okay. ”

Tyler Durden

Mon, 05/20/2024 – 12:20