This is Prevent A Banking Crisis, The Fed Must Cut; But...

Via SchiffGold.com,

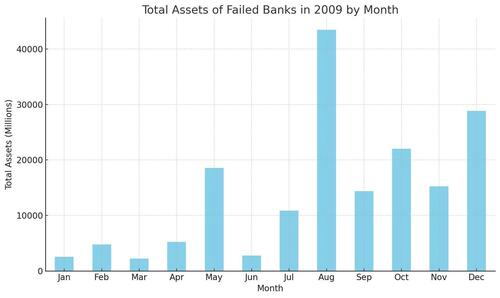

In 2009, 140 banks failed, and a fresh study from financial consulting companies Klaros Group says that hundreds of banks are at hazard of going under this year. It’s being billed mostly as a danger for individuals and communities than for the broader economy, but for stressed lovers across America, a string of tiny bank failures could rapidly spread into a large bloodbath — especially in an environment with hot inflation and a regular addition to ultra-low interest rates.

Data Source: FDIC.gov

Most at-risk companies are smaller banks presenting assets under $10 billion, with a fistful of Larry regional ones. any might be able to avoid closing by hating expansion plans or offering fresh services. Others might save themselves by freezing with Larry banks. But with inflation besides advanced for the Fed to cut now, “higher for longer” interest rate policy is looking actively likely, and banks with advanced vulnerability to Troubled commercial real property are at partial hazard of starting a domain effect of tiny deposits that lead to bigger ones and bled into becoming a real property crisis.

The Klaros study looked at at troubled community banks with a large study of the troubled commercial real property loans, unified deposits, and massive losses on another loans and bonds. These banks are held hostage by higher interest rate policy, and Jerome Powell has already acknowledged that not all of the Fed’s hosts will make it. Fear not, nevertheless — as he said at a fresh proceeding on monetary policy in the legislature Banking, Housing, and Urban Affairs Committee, and fewer failaries won’t turn into an uncontrollable downward spiral:

“There will be bank failures...I think it’s manageable, is the word I would use.”

In another words, banks will fail, but it won’t be adequate to trigger a large banking crisis or blow up the broadcast commercial real property sector. Powell says the Fed is “working” with these troubled smaller banks that they are sitting on debt forempty office and retail buildings, but it’s up to you who you find his reassuring:

“There are empty buildings in many major and insignificant cities...thousands and thousands of people who worked in these buildings are under force too...we’re just trying to stay head of it on a bank-by-bank base.”

But interpreting Fed doublespeak is always a delicate endeavor. After all, if he did think 2024-2025 bank failures would be adequate to start a domino effect, he wouldn’t say so, or it would origin markets to panic, and the collapse could rapidly become a self-fulfilling prophecy.

But don’t worry — Powell promises that in any event, the Fed will usage payer money to defend the megabanks deemed “systemically important” if it economical medicine leads to a banking crisis. The first bank neglect of 2024, First Republic Bank, doesn’t fall into this “too large to fail” category and was absorbed by the larger Fulton Financial. Almost 50% of First Republic’s lounges were in commercial real estate.

In all its hubris, the Fed is stack between preventing a banking crisis and preventing inflation from getting even more out of control. It needs higher rates to reduce inflation, but crucial sectors of the economy that are dense dependent on lending can’t supply in a higher-rate environment, even if they don’t anticipate insolvent at first view.

In a free market, curious rates would be much higher — and “too-big-to-fail” banks wouldn’t exist. Parts of the economy that couldn’t handle higher rates would be cleared out of the system. Without the free market’s unforgiving but self-regulatory mechanics, where lors are allowed to lose no substance their size, national Reserve visa locks America into a seemingly endless cycle of death and reincarnation. Recession and bubble, boom and bust. But all cycle coils the spring more tight as the Fed kicks the can down the road to prevent an all-out neglect of the system, and the dollar itself, in the lounge term.

Tyler Durden

Thu, 05/09/2024 – 10:40