"The Jobs marketplace Is Weakening, Inflation Has Picked Up And Growth Unexpectedly Sled"

By Rabobank

The Bank of England left the Bank Rate changed at 5.25% yesterday, but the clear signal from the evidence of votes, and politician Bailey, is that cuts Aren't far away. This time around the vote divided 7-2 in favour of holding (previously 8–1), with arch-dove Dhingra being joined by erstwhile hawk Ramsden in plumping for a cut.

The BOE’s Monetary Policy study led inflation forecasts, but the policy Summary warned on guarantees around the presence of advanced services inflation and the spotty ONS labour marketplace data. politician Bailey comments that a cut in June is “neither ruled out nor a fait accompli” while our own BOE watcher Stefan Koopman favors an August cut, owing to sticky services inflation and guarantees around the impact of the last 9.8% minimum weight decision.

So, the Bank of England is now in a akin place to the ECB, and a akin place to where the Fed was earlier in the year: cuts are coming, we just needed to see any more data to be estimated on the timing. In spending so much time talking about cutting rates before actually cutting them, central bankers are doing their best Abe Lincoln impersonation: “give me six hours to chop down a tree, and I will spend the first 4 sharpening the axe.“

A dovish Bank of England follows Sweden’s Rijksbank delivering a 25bps cut earlier in the week (the first in 16 years) and a 25bps cut from the Brazilian central bank yesterday (though 4 Board members wanted to cut by 50). The RBA does-it-up on Tuesday by keeping the cash rate changed at 4.35% and managing their neutral bias – despite a large upside surprise in inflation in Q1 and half-percentage point upward revisions to their inflation forecasts for the reminder of this year. We think the RBA’s ‘hold and hope’ strategy will eventual get waylaid by economical reality and that they will end up hiding more this year, albeit reluctantly.

Banxico might have been the close thing to a Hawkish central bank this week. They opted to pause the cutting cycle that was initiated in March, while revising inflation forecasts constantly higher and informing of persistence in inflationary shocks. USDMXN dropped below 16.80 following the gathering despite tiny gain in the DXY index. Nevertheless, Rabobank’s Christian Lawrence and Molly Schwartz are expecting Banxico’s policy rate to proceed falling later in the year, eventual hitting 10% by Christmas.

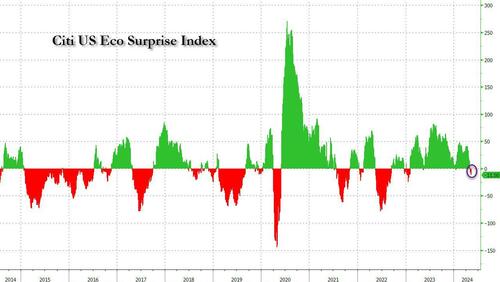

Over in the United States we saw a continuation of the subject established by a soft non-farm payrolls study last Friday that the US jobs marketplace may beginning to crack. Initial jobless claims this week printed at 231,000, well up on the expected 212,000 and last week’s upwardly-revised 209,000. This follows a fresh run of soft data, including the lacklustre payrolls report, below results JOLTS occupation openings, and ISM reports showing employment contract for both the manufacturing and services sectors.

While the laboratory marketplace is starting to look creamy, the prices paid components of these ISM reports pumped higher. This chimes good with a strong run of PCE and CPI data, which we might see continued next week erstwhile we get the April PPI and CPI reports for the United States. Could another upside surprise be on the cards there? [ZH: a downside surprise is far more likely]

So, The jobs marketplace looks to be weathering, inflation has picked up and growth unexpectedly sled to just 1.6% annualized in Q1 figures reported the week before last. Nevertheless, Jay Powell isn’t married. He late told reporters that he couldn’t see the ‘stag’ or the ‘flation’ in the economy at the moment.

The BOE and the ECB may be connected 1 erstwhile president in softening us up for rate cuts, but in light of the fresh run of data it stretches credulity to propose that Powell is channelling another: “Father, I cannot tell a lie...’

While the economical image apps to be softening in North America, in Europe things seemed to turn for the better this week. PMIs indicated a fast rate of expansion for Spain, France and Germany, and Italian manufacture besides remains in expansion (albeit at a lightly reduced rate). German mill orders restored dreadful, but both imports and exports shown unexpected strength. French wage growth accredited and German industrial production was little bad than felt. All of this follows on from pager than expected Q1 growth figures for the Eurozone last week.

Europe might be looking better, but it isn’t time to break out the mutiny just yet. Growth is inactive weak, and it would be a brave call to propose that inflation has been routed – even if it may be in retreat at the moment. There’s besides plenty of possible for further shocks. Just this morning we Saw news that Joe Biden plans to impose tariffs on Chinese EVs and another strategical sectors as early as next week. specified moves rise the hazard of China dumping these products into another markets (like Europe), which might advance action from the Europeans to defend already fragile German industry.

There’s besides the issue of the Israel-Hamas (/Hezbollah/Iran) war bubbling distant in the background. Brent crude has stabilized around $83-84/bbl after the fresh tit-for-tat between Israel and Iran momentarily petered-out, but tensions stay advanced and the war is moving into a fresh phase that introduces fresh powerful catalysts for regional potshots.

Israel this week cut off the crossing from Rafah into Egypt as a precursor to a ground offensive. Hamas tried to accept a batchfire deal that Israel hadn’t offered. Joe Biden Wound-back long moving bipartisan support of Israel by thrilling to halt ships of offensive weapons if Israel pushes into Rafah. That later improvement was almost absolutely elegantly-driven, with the campus youth vote, and the large Muslim population in Michigan of cruel import to Biden’s Chances of re-election. Netanyahu restores undeterred, declaring that “If we must, we will fight with our fingers.’

So, all in all, it was another week where there were plenty of problems that we can point to, but both stocks and bonds gone higher (at least as of time of writing). possibly there is any fact to an reflection a merchant erstwhile made to me: “Bears sound smart, but bulls make money

Tyler Durden

Fri, 05/10/2024 – 18:05