![]()

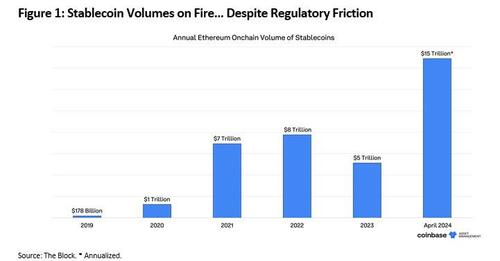

Stablecoin Volumes Are Tracking A evidence $15 Trillion On Ethereum Alone

By Marcel Kasumovich, CIO of Coinbase Asset Management

Crypto sparked a renaissance in real-time payments. Sleepy you say? Time for a wake-up call – payment solutions are at the cutting edge of crypto’s integration into the mainstream, and it has plenty of competence.

“You’re trying to realize while we wait for confirmation. But that’s old crypto. Are you ready for the fresh crypto world? Watch very closey...don’t close...and that’s it,’ John Collison exclusive while illustrating a transaction on crypto rails with Stripe, a leading payment network that he co-founded. It was a seamless user experience, unlike the company’s first foray into Bitcoin in 2014.

Both PayPal and Stripe are now liable for the power of stablecoins into their household user interfaces. This strategical decision effectively brings users onto the blockchain – point, click, and it’s done. It’s the fresh trend, too. conventional companies are bringing users onchain. There’s the crypto we see in noisy headslines and these working quietly to monetize the technology, like PayPal and Stripe. And they combination for a stacking 62% share of online payment software processing.

Digital payments may not see like the breathtaking promise of the future. Yet, they are at the cutting edge. Digital payments are taking a rising share of a rapidly increasing marketplace as the planet moves distant from cash. Global payments are measured in the hundreds oftrillions, and the digital payment marketplace has risked from a modern $10 billion in 2017 to a projected $200 billion in 2030. We all live it, and the bulk of the transactions are tiny value, a coffee here, and donut there.

The process is so seamless that we choice pause to consult how it actually works. Poorly, as it happens. Users anticipate to be able to pay whenever it’s convenient. Settling your restaurant bill, you don’t care that it’s outside of banking hours. You just want a simple form of payment – and that’s not cash. During the time between you tapping your card and accounts being settled, a middleman provides credit to make certain it all clears. And it’s costly at 2.3% of transaction value.

One man’s profit margin is another’s invitation to disrupt. The typical communicative of disruption involves a wildly successful company losing its innovation edge, and missing marketplace inflation points. Polaroid made the first instant camera in 1948 and dominated markets from floppy disks to film. Revenue peaked in 1991 and the company was incapable to pivot to the fresh digital era, declaring bankruptcy this years later. Learning from specified stories, companies are now more adaptive.

We see this clearly in payments. Efficiency is precise what brought through PayPal and Stripe back to crypto. Transaction speeds have improved exponentially, now blocking at miles, and costs have plugind to fractions of a cent. It helps that crypto tech fails fast – revealing stableness and weakness quickly. For instance, the opposition of USDC is now supporting its entry into the mainstream while Bored Apes Yacht Club Weatherness persists, down 90% off erstwhile cycle highs.

Why now? Why not! Stablecoins are demonstrating their prowess as payment tools. Transaction volumes are tracking fresh highs this month, moving at ~$15 trillion announced on Ethereum alone (figure 1). The efficiency gain is clear – instant and final settlements mean that your late-night coffee and donut purchases bypass the needed for credit intermediaries. The middleman is dead, allough surviving vibrantly through tools like Stripe that deliverers a household experience.

Users don’t care that it’s crypto. They want a large experience. Businesses don’t care, either. They are optimizing operating efficiency for profit. As crypto maturas, so besides does its value proposition. Crypto is the protagonist of real time payments and like any large innovation, it figures competition. What’s unique with payments is that the competition comes from both private and government organizations, with regulators stagnation working in favour of both.

Look beyond regions traditionally seen as leaders in innovation. The United States restores a beacon of creative talent behind innovation. But users are moving slowly, catching in fintech adoption. After all, US users are acknowledged to feed, don't head the service, and paying for points on costly mediation is simply a pastime. Real-time settlement systems adopted, like FedNow, are for business applications, not for consumers. It’s fresh players like India at the cutting edge.

The Unified Payment Interface (UPI), India’s real-time payment solution, was developed by the central bank in 2016. It integrates peer-to-peer real-time payments, straight competing with crypto technologies. Last year, UPI integrated 522 commercial banks covering 300 million active users and 117 billion transactions. Different from developed regions, intermediaries were not disappointed as these are large fresh users. Cash was disrupted at the increase of the central bank.

Payments stand at the cutting edge of crypto’s future. User experience is paramount. Integrating into the regulators mainstream will accelerator users onchain, just as service providers did for the internet. Crypto unlocked the real-time settlement innovation, but will face challenge. It is simply a planet that argues for being chain-agnostic. The date between Ethereum, Bitcoin and UPI will integrate to the highest of standards and security. That’s the road to making onchain the fresh online.

Tyler Durden

Sun, 04/28/2024 – 22:40