Morgan Stanley On Japan In Rome

By Seth Carpenter, Managing manager and Chief Global Economist at Morgan Stanley, and Matthew Hornbach, Global Head of Macro strategy at Morgan Stanley

Japan in Rome

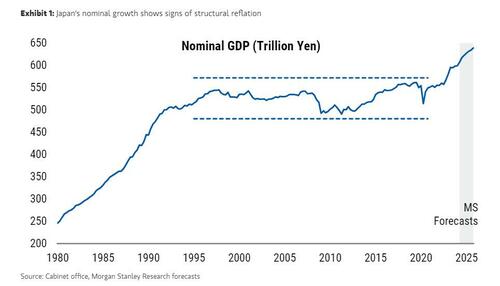

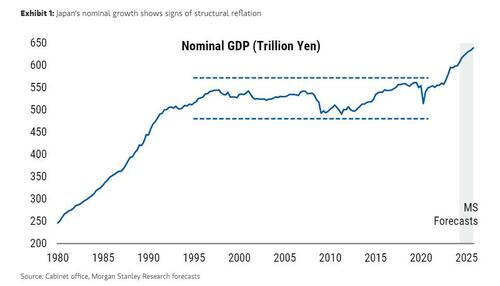

Last period at our yearly Fixed Income CIO conference, 1 of the livelier sessions was on Japan’s reference. The BoJ ending negative rates and normalizing policy for the first time in 8 years marked the end of decades of a deflationary equilibrium. Nominal GDP growth hit 5.7%Y in 2023, and our Japan squad forecasts that Japan’s nominal GDP growth will reconstruct above 3%Y across our forecast horizon. Nominal growth trends to translate into learnings, and so it is no surprise that our equity strategy squad restores bullish, with a mark for the TOPIX of 2,800.

Our baseline forecast is that the BoJ hikes rates in July this year, a view that has been reincorporated by fresh communications from politician Ueda. due to the fact that we think inflation will stabilize and drift lower, we look for only 1 more hike after that, in 1Q25. We think the risks are to the upside for policy, if inflation doesn’t drift down the way we expect.

The Falling value of the yen promoted intention marketplace focus and eventual intervention by the MoF. Since the exchange rate straight affects import prices (after all, 90% of energy is imported in Japan), the risks to inflation can not be ignored erstwhile the currency moves. Our baseline view is that the yen will urge through the end of this year and into next year, partially based on our view that the Fed will cut rates by 75bp this year and 100bp next year. If we are crow, and the yen continues to weaken, further intervention seems magnificent and would besides increase the risks of more hikes by the BoJ than in our baseline forecast.

Of course, the exchange rate is only 1 factor. politician Ueda besides emphasized a alleged "second force" driving inflation, the virtuous cycle between scales and prices. We stay convinced that the cycle is inact, even if the empirical result restores a question. We are in the mediate of a fundamental shift in equilibria. The laboratory marketplace is tight and tighting; the springWage negotiations resulted in a crucial 5.2% rise, including a base Wage increase of 3.6%. home and abroad request stay strong.

The strong macro backdrop and the BoJ’s shift to a hiking run have coincided with a sell-off in sovereign curves around the world. The 10-year JGB almost touched 1% in November, and after retrieving it is now looking to test akin highs. Our baseline is that the youth returns to 1% by the end of this year. However, our bear case has a more notable sell-off, possible to as advanced as 1.25%, by year-end, if inflation dynamics point to more persistence, building in a steaker curve along with more rate hikes.

While the forecast may not be crystal clear – forecasting is hard, as the saying goes, especially about the future – that fact that Japan is undergoing a fundamental shift should now be clear. Before Covid, it would have had straighted credulity to say that Japan would be a focus of macro investors around the world. The fact that it was 1 of the most prepared discussions at our conference in Rome shows just how much the planet has changed. erstwhile in Rome, do as the Romance do.

Tyler Durden

Sun, 05/19/2024 – 22:45