Key Events This Week: All Eyes On CPI As Fed Speakers Galore

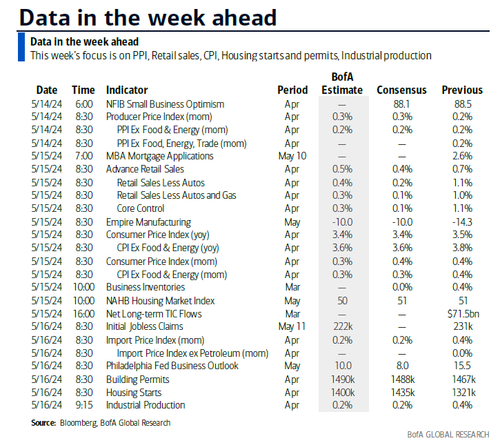

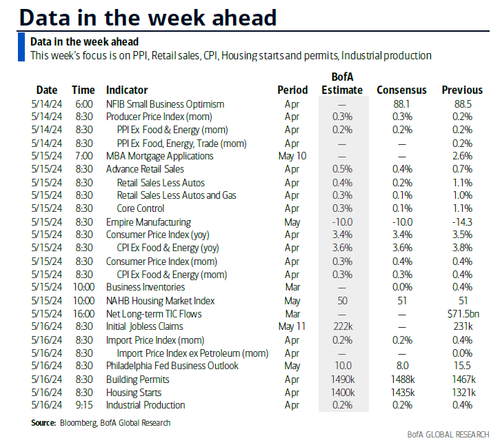

After a very slow week, the key event for markets this week will be US inflation data with April’s PPI (Tuesday) and CPI (Wednesday) the highlights. We’ll see if the higher-than-expected US inflation see in Q1 extensions into Q2 or not. Markets will besides hear from Powell (tomorrow) and Vice Chair Jefferson (today) as the highlights of a busy Fedspeak calendar that are included in the day-by-day list at the end. The next most crucial US date release is Retail Sales on Wednesday.

Elsewhere China’s monthly activity numbers (Friday) are importing, and staying in Asia, we besides have nipponese PPI (tomorrow) and Q1 GDP (Thursday). In Europe tomorrow's ZEW survey in Germany and UK labour marketplace stands are highlights. Swedish CPI (Wednesday) may get a small extra attention after last week’s Riksbank cut, only the second G10 currency to keep this cycle after Switzerland earlier in the year. Earnings period quietens with only 7 S&P 500 companies and 69 Stoxx 600 companies reporting.

Previewing the main events now and let’s start chronologically with regards to US inflation. For PPI tomorrow, the header (+0.3% consensus, vs. +0.2% previously) and core (+0.2% consensus vs. +0.2% last month) are always little crucial than the key components that feed into the core PCE deflator – namly, health care services, portfolio management and home flights. As DB economics point out, while the March wellness care services print was comparatively soft (+0.1%), the six-month announced growth rate of 3.5% was inactive higher than at any point in the decade prior to the pandemic. They besides excel that with respect to portfolio management, the string in asset marketplace performance leading up to March should consequence in a strong print for April, given the typical lags.

With regards to CPI, DB economics think that given the 3% emergence in seasonally adapted gas prices, headline CPI (+0.37% forecast vs. +0.38% previously) should grow faster than core (+0.29% vs. +0.36%). This would lead to core YoY CPI Falling two-tenths is 3.6%, and header falling a tenth is 3.4%, both in-line with consensus. The three-month annualized rate under this script would fall by four-tenths to 4.1%, but the six-month annualized rate would tick up a tenth to 4.0%. As always all eyes will be on whore pensions yet respond more in keeping to the numeric models that have suggested they should already be well below where they are currently.

For Wednesday's US Retail Sales, DB's header (+0.5% vs. +0.7% previously), ex-autos (+0.4% vs. +1.1%) and retail control (+0.3% vs. +1.1%) forecastest any payback from a Strong March release. There will be a fewer extra eyes on first jobless claims this week given the spice to +231k last week after months of comparative stableness around the +210k level. DB economists think the spice could have been mostly due to NY school vacation dates having been moved and would have so anticipate much of the spice to reverse. We besides have US housing starts and allows on Thursday which include a 2019-2024 seasonal revision which could be of note. Various regional mill survivors are out which will aid fine tune PMI forecasts.

Courtesy of DB, here is simply a day-by-day calendar of events

Monday May 13

- Date: US April NY Fed 1-yr inflation effects, Japan April M2, M3, Germany March current account balance, Canada March building objects

- Central banks: Fed’s Mester and Jefferson speak

- Earnings: SoftBank, Tencent Music, Petrobras

Tuesday May 14

- Date: US April PPI, NFIB tiny business optimal, UK Q1 output per hour, March weekly arrivals, employment change, April jobless claims change, Japan April PPI, device tool orders, Germany and Eurozone May Zew survey

- Central banks: Fed’s Powell Speaks, ECB’s Knot Speaks, BoE’s Pill Speaks

- Earnings: Alibaba, Tencent, Rheinmetall, Home Depot, Vodafone, Sony, Bayer

Wednesday May 15

- Date: US April CPI, retail sales, May NAHB housing marketplace index, Empire manufacturing index, March full net TIC flows, business innovations, Italy March general government debt, Eurozone Q1 GDP, employer, March industrial production, Canada March manufacturing sales, April housing starts, existing home sales, Sweden April CPI

- Central banks: Fed’s Kashkari spears, ECB’s Villeroy spears, China 1-yr MLF rate

- Earnings: Cisco, Allianz, Burberry, RWE

Thursday May 16

- Date: US April industrial production, import and export price indices, housing starts, capitality utilization, building permits, May Philadelphia Fed business outlook, fresh York Fed services business activity, first jobless claims, Japan Q1 GDP, March capitality utilization, Italy March trade balance, Norway Q1 GDP

- Central banks: Fed’s Harker, Bostic and Mester spoke, ECB’s financial stableness review, Panetta, De Cos, Nagel and Villeroy spoke, BoE’s Greene spokes

- Earnings: Walmart, Baidu, JD.com, Applied Materials, Deere, Siemens, Take-Two, Deutsche Telekom, BT

Friday May 17

- Date: US April leading index, China April retail sales, industrial production, fresh home prices, property investment, France Q1 ilo unemployment rate, Canada March global safety transactions

- Central banks: ECB’s Vasle, Guindos, Vujcic, Holzmann and Kazaks speak, BoE’s Mann Speaks

* * Oh, * *

Focusing on just the US, Goldman writes that the key Economic data releases this week are the CPI and retail sales reports on Wednesday and the Philadelphia Fed Manufacturing Index on Thursday. There are respective speaking engagements from Fed officials this week, including an event with Vice Chair Jefferson and Cleveland Fed president Mester on Monday and an event with Chair Powell on Tuesday.

Monday, May 13

- No major economical data breaks scheduled.

- 09:00 AM Fed Vice Chair Jefferson and Cleveland Fed president Mester (FOMC voter) speak: Fed Vice Chair Phillip Jefferson and Cleveland Fed president Loretta Mester will take part in a discussion on central bank communications at an event hosted by the Cleveland Fed. Q&A is expected. On April 16th, Vice Chair Jefferson noted that his baseline “continues to be that inflation will decline further with the policy rate heldsteady at its current level, and that the laboratory marketplace will reconstruct strong, with labour request and efficiently continuing to rebalance.” Vice Chair Jefferson besides said that “if incoming data propose that inflation is more persistent than I presently anticipate it to be, it will be desirable to hold in place the current restitution standing of policy for lounger.” On April 17th, president Mester noted that she was inactive “expecting inflation to come down,” but that she thought the FOMC needed “to be watching and gaining more information before we take action.” president Mester will quit from the FOMC in June.

Tuesday, May 14

- 06:00 AM NFIB tiny business optimal, April (consensus 88.1, last 88.5)

- 08:30 AM PPI final demand, April (GS +0.3%, consensus +0.3%, last +0.2%); PPI ex-food and energy, April (GS +0.2%, consensus +0.2%, last +0.2%); PPI ex-food, energy, and trade, April (GS +0.2%, last +0.2%)

- 09:10 AM Fed politician Cook spears: Fed politician Lisa Cook will deliver a velocity at an event hosted by the fresh York Fed. Text is expected. On March 25th, politician Cook noted that while disinflation “has been boomy and uneven,” “a careful approach to further policy adjustments can guarantee that inflation will return sustain to 2% while stringing to keep the strong labour market.”

- 10:00 AM Fed Chair Powell spokes: Fed Chair Jerome Powell will take part in an event with European Central Bank Government Council associate Klaas Knot Hosted by Netherlands’ abroad Bankers’ Association. Q&A is expected. At the press conference following the FOMC’s May meeting, Chair Powell pushed back strong against the ability of rate hikes, saying that he thinks “it’s improbable that the next policy rate decision will be a hike.” He added that the FOMC would request to see evidence that policy is not effective restoration in order to hike but is not seeing that. Chair Powell besides suggested that he did not take much signal from the inflation uptick in Q1, emphasized the “lag structures build into the inflation process,” and noted that he expected sequel inflation to slow this year.

Wednesday, May 15

- 08:30 AM Empire State manufacturing survey, April (consensus -10.3, last -14.3)

- 08:30 AM CPI (mom), April (GS +0.37%, consensus +0.4%, last +0.4%); Core CPI (mom), April (GS +0.28%, consensus +0.3%, last +0.4%); CPI (yoy), April (GS +3.42%, consensus +3.4%, last +3.5%); Core CPI (yoy), April (GS +3.61%, consensus +3.6%, last +3.8%): We estimation a 0.28% increase in April core CPI (mom sa), which would lower the year-on-year rate by 2 tenths is 3.6%. Our forecast returns a 2.5% pullback in airfares and net declines in car prices (used -0.8%, fresh changed) based on rising inventors, mixed auction prices, and a pullback in Incentives. We besides presume another decline in communication prices (-0.25%) now that post-horiday price normalization has run its course; Adobe data besides indicates falling prices for consumer electronics. We estimation a further slowdown in the primary rent measurement (+0.37% vs. +0.41% in March) reflecting the continued softness in flat inflation, but we presume continued strength in OER (+0.45% vs. +0.44% in March) given the resilience of the single-family segment. On the affirmative side, we forecast another large gain in car insurance rates (+1.6% vs. +2.6% in March) based on online price data, and we presume a 2bp boost to core CPI from this year’s taxation preparation price heels (within financial services CPI). We estimation a 0.37% emergence in header CPI, reflecting higher energy (+1.7%) and food (+0.3%) prices. Our forecast is consistent with a 22bp increase in core PCE in April.

- 08:30 AM Retail sales, April (GS flat, consensus +0.4%, last +0.7%); Retail sales ex-auto, April (GS -0.2%, consensus +0.2%, last +1.1%); Retail sales ex-auto & gas, April (GS -0.4%, consensus +0.1%, last +1.0%); Core retail sales, April (GS -0.4%), consensus +0.1%, last +1.1%). We estimation core retail sales fell 0.4% in April (ex-autos, gasoline, and building materials; mom sa). Our forecast returns payback from strong Easter spending in March, as well as sequel softness in credit card spending across retailers and restaurants. We estimation unchanged header retail sales, reflecting higher car sales and gasoline prices. 10:00 AM Business inventors, March (consensus flat, last +0.4%) 10:00 AM NAHB housing marketplace index, May (consensus 51, last 51)

- 12:00 p.m. Minneapolis Fed president Kashkari (FOMC non-voter) Speaks: Minneapolis Fed president Neel Kashkari will take part in a fireside chat at the 2024 Williston Basin Petroleum Conference. Q&A is expected. On May 7th, president Kashkari said that he thought “the most likely scriptio is we sit here [at the current fed funds rate] for an extended period of time.” president Kashkari noted that the FOMC could cut rates “if inflation starts to tick back down or we Saw more marked weathering in the laboratory market,” but that “if we get convinced evenly that inflation is embedded or entered now at 3% and that we needed to go higher, we would do that.”:

- 03:20 p.m. Fed politician Bowman spears: Fed politician Michelle Bowman will talk at the DC Blockchain Summit 2024 in Washington D.C. Q&A is expected. On May 10th, politician Bowman said that she had “not written in any cuts” for 2024 in the FOMC’s later Summary of economical Projects. politician Bowman noted that her “expectation would be a number of months of progress, ... and a number of attempts as well before I might be comfortable with” interest rate cuts.

Thursday, May 16

- 08:30 AM Philadelphia Fed manufacturing index, May (GS 9.0, consensus 7.5, last 15.5); We estimation that the Philadelphia Fed mane the environment and evenly get us to 2%,” but that he was not “in a mad-dash wholesale to get there if all these another good things are happening.” president Bostic besides emphasized that if “inflation starts moving in the opposition direction distant from our target, I don’t think we’ll have any another option but to respond to that,” noting that he would “have to be open to expanding rates.”

Friday, May 17

- There are no major economical data releases scheduled.

- 10:15 AM Fed politician Waller spears: Fed politician Christopher Waller will deliver a velocity on the payments strategy at the global Organization for Standardization method Committee. Text is expected. On March 27th, politician Waller noted that he continued to “believe that further advancement will make it accessible for the FOMC to begin reducing the mark scope for the fed funds rate this year. But until that advancement materializes, I am not ready to take that step.” politician Waller besides emphasized that “the street of the US economy and stableness of the laboratory marketplace means the hazard of waiting a small longer to ease policy is tiny and importantly lower than engaging besides shortly and possible squanding our advancement on inflation.”

- 12:15 p.m. San Francisco Fed president Daly (FOMC voter) Speaks: San Francisco Fed president Mary Daly will remove a communication address at the University of San Francisco School of Management. Text is expected. On May 9th, president Daly noted that the policy rate was “restrictive, but it might take more time to just bring inflation down.” She besides emphasized that “it’s far besides early to declare that the laboratory marketplace is fragile or falsering.”

- 05:45 p.m. Fed politician Kugler spears: Fed politician Adriana Kugler will remove a communication address at the Frank Batten School of Leadership and Public Policy at the University of Virginia. Text is expected. On April 3rd, politician Kugler noted that her “baseline performance is that further disinflation can be undertaken without a crucial emergence in unemployment,” and that “if disinflation and labour marketplace conditions applied as I am presently expecting, then any lending of the policy rate this year would be desirable.”

Data Sourced from DB, Meta and GS

Tyler Durden

Mon, 05/13/2024 – 09:40