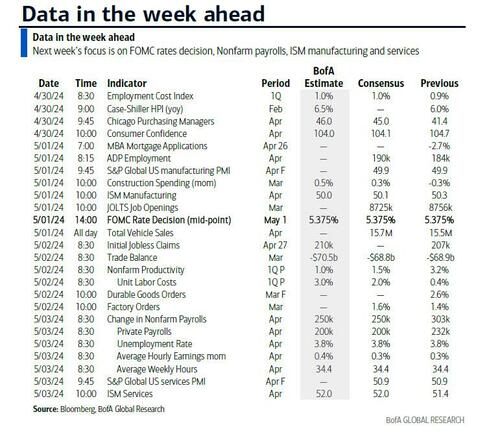

Key Events This utmost Busy Week: Fed, Treasury Refunding, Jobs, JOLTS, ISM And Tons Of Earnings

As DB’s Jim Reid notes, with just 2 days left in a rollercoaster April for markets – and FX – last week actually Saw the best week for the S&P 500 (+2.67%) and NASDAQ (+4.23%) since November, following respective weeks of declines, as earlys give markets a boost even if the US inflation data was on net Worrying. And while the period is inactive over, the fresh week is just starting and as Reid notes, it’s sharing up an exclusive busy week of crucial events.

The FOMC on Wednesday is the ambient item of the week, but we besides have payrolls on Friday to look forward to. DB anticipate a more hawkish-learning Fed this week. While our economics effect the Committee will keep an easing bias, they do anticipate the message and press conference to echo Chair Powell’s view that company inflation prints propose it will take longer to gain assurance about disinflation. The press conference will befascinating to see the nuances in Powell’s responses as he justifys a likely changed easier white, even if the rhetoric is more Hawkish, in the face of rising inflation.

In terms of the jobs study on Friday, our US economics see paying +240k in April (consensus +250k), down from +303k in March. The consensus results the unemployment rate and the hourly learnings growth rate to stay at 3.8% and +0.3% MoM, relatively, even DB results the form to tick up a tenth. Overall the marketplace sees a solid report.

Other key data in the US includes consumer assurance tomorrow, the manufacturing ISM, JOLTS, and ADP on Wednesday, and the services ISM on Friday. We besides see the later US Treasury Quarterly refunding cancellation on Wednesday, after the borrowing estimation is due today. This was a large pivot point for global markets back in August (negative) and October (positive) but since then a message not to increase auction sizes has reduced its import.

Finally in the US, learnings period maintains its highest pace as 174 study in the S&P versus 180 last week with Amazon (Tuesday) and Apple (Thursday) the ambient highlights. Meanwhile, 66 Stoxx 600 companies will study this week.

In Europe, preliminary CPI reports for Germany and Spain today, and the Eurozone next day will have quite a few importance for the June ECB gathering and who we will see the first cut. Our European economists preview the release here. For the Eurozone, they anticipate the header HICP to fall one-tenth to 2.31% yoy, its value value since August 2021 and see core inflation slowing further to 2.45% yoy, 0.50pp lower than in March 2024. Staying in Europe the latest GDP data for Germany, France, Italy and the Eurozone are due tomorrow. In Asia, various China PMIs (tomorrow) will be a large focus and in Japan, respective key economical indicators are besides due, including industrial production and Labour marketplace data volume.

Day-by-day calendar of events:

Monday April 29

- Date : US April Dallas Fed manufacturing activity, Germany April CPI, Eurozone April services, industrial and economical confidence

- Earnings : PetroChina, China Construction Bank, BYD, NXP Semiconductors, Domino’s Pizza, Paramount Global

- auctions : US Treasury borrowing estimates

Tuesday April 30

- Date : US Q1 employment cost index, February FHFA home price index, April MNI Chicago PMI, Dallas Fed services activity, Conference Board consumer confidence, UK March net consumer credit, mortgage approvals, M4, April Lloyds business barometer, China April authoritative PMIs, Caixin manufacturing PMI, Japan March retail sales, job-to-applicant ratio, jobless rate, industrial production, housing starts, Italy Q1 GDP, March hourly scales, April CPI, Germany Q1 GDP, April unemployment claims rate, France Q1 GDP, consumer spending, April CPI, April CPI, April CPI, Canada February GDP, fresh Zea Denmark Denmark

- Central banks : BoE’s APF report

- Earnings : Amazon, Eli Lilly & Co, Samsung, Coca-Cola, AMD, McDonald’s, Stryker, Starbucks, Mondelez, Mercedes-Benz Group, Volkswagen, PayPal, adidas, Diamondback Energy, Restaurant Brands, Pinterest, Vonovia, Covestro, Caesars Entertainment

Wednesday May 1

- Date : US March JOLTS report, construction spending, April full vehicle sales, ISM index, ADP report, Canada April manufacturing PMI

- Central banks : Fed’s decision

- Earnings : Mastercard, Qualcomm, Pfizer, KKR, GSK, Marriott, Estee Lauder, DoorDash, Corteva, Haleon, Devon Energy, Barrick Gold, eBay, Albemarle, Etsy

- auctions : US quarterly refunding cancellation

Thursday May 2

- Date : US Q1 unit labour costs, nonfarm productivity, March trade balance, mill orders, first jobless claims, Japan April monetary base, consumer assurance index, Italy March PPI, April manufacturing PMI, fresh car registrations, budget balance, Canada March global merchandise trade, Switzerland April CPI

- Central banks : BoJ minutes of the March meeting

- Earnings : Apple, Novo Nordisk, Shell, Linde, ConocoPhillips, Booking, Cigna, Regeneron, Apollo, Pioneer, Universal Music Group, Block, Ares, Moderna, Blue Owl, Vestas, AP Moller – Maersk, Orsted, ArcelorMittal, Live Nation Entertainment, DraftKings

- Other : UK local elections, OECD economical outlook

Friday May 3

- Date : US April jobs report, ISM services, UK April authoritative reserves changes, Italy March unemployment rate, France March industrial production, budget balance, Eurozone March unemployment rate, Canada April services PMI, Norway April unemployment rate

- Earnings : Hershey, Daimler Truck, Cheniere Energy

* * Oh, * *

Looking at just the US, Goldman writes that The key economical data releases this week are the employment Cost Index on Tuesday, ISM manufacturing and JOLTS occupation openings on Wednesday, and the employment study on Friday. The May FOMC gathering is on Wednesday. The post-meeting message will be released at 2:00 p.m. ET, followed by Chair Powell’s press conference at 2:30 PM. Treasury will release its Q2 financing estimates on Monday and the Quarterly Refunding message on Wednesday.

Monday, April 29

- 10:30 AM Dallas Fed manufacturing activity, April (consensus -11.3, last -14.4)

Tuesday, April 30

- 08:30 AM employment cost index, Q1 (GS +0.9%, consensus +1.0%, last +0.9%): We estimation the employment cost index rose by 0.9% in Q1 (qoq sa), which would lower the year-on-year rate by 2 tenths to 4.0% (nsa youth). Our forecast returns determination in the Atlanta Fed wage tracker and in average hours of production and nonsupervisory workers. We besides anticipate a slow package of ECI growth among unionized workers, following the 1.7% spice in Q4 (SA by GS, not announced). On the affirmative side, we presume ECI benefit growth picks back up to 0.9% (vs. 0.7% in Q4), reflecting expanded benefit offerings at the start of the year.

- 09:00 AM FHFA home price index, February (consensus +0.1%, last -0.1%)

- 09:00 AM S&P Case-Shiller 20-city home price index, February (GS +0.07%, consensus +0.10%, last +0.14%)

- 09:45 AM Chicago PMI, April (GS 46.4, consensus 45.0, last 41.4): We estimation that the Chicago PMI rose by 5pt to 46.4 in April, reflecting the rebel in global manufacturing activity.

- 10:00 AM Conference Board consumer confidence, April (GS 104.3, consensus 104.0, last 104.7

Wednesday, May 1

- 08:15 AM ADP employment change, April (GS +185k, consensus +180k, last +184k): We estimation a 185k emergence in ADP payroll employment in April, reflecting a solid underlying package of occupation growth and a possible boost from residual seasonality: the ADP measurement has picked up in April comparative to Q1 in 4 of the last years exclusive 2020.

- 09:45 AM S&P Global US manufacturing PMI, April final (consensus 49.9, last 49.9)

- 10:00 AM Construction spending, March (GS +0.8%, consensus +0.3%, last -0.3%)

- 10:00 AM JOLTS occupation openings, March (GS 8,650k, consensus 8,680k, last 8,756k): We estimation that JOLTS occupation openingsfell by 0.1mn to 8.65mn in March, reflecting the pullback in online occupation posts.

- 10:00 AM ISM manufacturing index, April (GS 50.8, consensus 50.1, last 50.3): We estimation the ISM manufacturing index rose by 0.5pt to 50.8 in April, reflecting the return in global manufacturing activity. Our manufacturing tracker rose 1.5pt is 49.9.

- 02:00 p.m. FOMC statement, April 30-May 1 meeting: As discussed in our FOMC preview, the upside inflation surprise over the last 3 months has died the first cut and narrated the way for the FOMC to cut at all this year. We have not changed our large image inflation view due to the fact that the surprises look idiosyncratic, the categories that are inactive hot reflect lagged catch-up alternatively than current cost pressures, and the key pills of the disinflation narratic stay intact. We anticipate the next fewer inflation reports to be softer and have thereforestack with our forecast of cuts in July and November, but even average upside forecasts could hold cuts further.

- 05:00 p.m. Lightweight motor vehicle sales, April (GS 15.8mn, consensus 15.7mn, last 15.5mn)

Thursday, May 2

- 08:30 AM Trade balance, March (GS -$69.0bn, consensus -$69.2bn, last -$68.9bn)

- 08:30 AM Nonfarm productivity, Q1 preliminary (GS +0.8%, consensus +0.8%, last +3.2%); Unit laboratory costs, Q1 preliminary (GS +3.5%, consensus +3.3%, last +0.4%): We anticipate nonfarm productivity growth of +0.8% (qoq saar) in the Q1 preliminary reading. We anticipate unit labour costs—compensation per hr divided by output per hour—to grow 3.5% in the Q1 preliminary reading, which would increase the year-over-year rate to +4.2%.

- 08:30 AM first jobless claims, week ended April 27 (GS 215k, consensus 210k, last 207k): Continuing jobless claims, week ended April 20 (consensus 1,798k, last 1.781k)

- 10:00 AM mill orders, March (GS +1.6%, consensus +1.6%, last +1.4%); Durable goods orders, March final (consensus +2.6%), last +2.6%); Durable goods orders ex-transport, March final (last +0.2%); Core capital goods orders, March final (last +0.2%);Core capital goods ships, March final (last +0.2%)

Friday, May 3

- 08:30 AM Nonfarm payroll employment, April (GS +275k, consensus +250k, last +303k); Private payroll employment, April (GS +225k, consensus +198k, last +232k); Average hours earlys (mom), April (GS +0.20%, consensus +0.3%, last +0.3%); Average hours, April (GS +3.95%, consensus +4.0%, last +4.1%); Unemployment rate, April (GS 3.8%, consensus 3.8%, last 3.8%); labour force participation rate, April (GS 62.7%, consensus 62.7%, last 62.7%): We estimation nonfarm payrolls rose by 275k in April (mom sa), reflecting a favourite evolution in the April seasonal factors and a continued boost from above-normal immigration. large Data measures were mixed but mostly indicate a solid or strong package of occupation gain, and our layout tracker continues to indicate that the package of layoffs is low. We estimation that the unemployment rate edged down but was unchanged on a rounded base at 3.8%, reflecting a emergence in household employment and flat-to-up labour force participation (at 62.7%). Foreign-born unemployment normalized in March, falling harply by 261k (SA by GS) and limiting the view for further declines in April. We estimation average hourly earlys rose 0.20% (mom sa), which would lower the year-on-year rate from 4.14% to 3.95%. Our forecast reflections waning weight pressures and a nearly 10bp drag from calendar effects (mom sa).

- 09:45 AM S&P Global US services PMI, April final (consensus 50.9, last 50.9)

- 10:00 AM ISM services index, April (GS 52.1, consensus 52.0, last 51.4): We estimation that the ISM services index rose 0.7pt to 52.1 in April. Our non-manufacturing survey tracker edged up 0.3pt to 52.1.

- 07:45 p.m. Chicago Fed president Goolsbee (FOMC non-voter) spears: Chicago Fed president Austan Goolsbee will participate in a panel discussion at the Hoover Institution. A Q&A is expected. On April 19, Goolsbee said, “Right now, it makes sense to wait and get more clarity before moving [rates].” He added, ‘So far in 2024, that advancement on inflation has stood. You never want to make besides much of 1 month’s data, especially inflation, which is simply a noisy series, but after 3 months of this, it can’t be dismissed.”

- 08:15 p.m. fresh York Fed president Williams (FOMC voter) Speaks: New York Fed president John Williams will talk in a panel discussion at the Hoover Institution. Speech text and a Q&A are expected. On April 18, Williams said, “I definitely don’t feel rgency to cut interest rates...I think interest rates will request to be lower at any point, but the timing of that is driven by the environment.” He added, “We have a strong economy... which means the rates we have haven’t caused the environment to slow besides much.”

Source: DB, Goldman

Tyler Durden

Mon, 04/29/2024 – 10:40