JPY Plunges To Fresh 34-Year-Lows After BoJ Does Nothing... Again

Having already lost more than 10% of its value versus the US dollar this year, the yen plunged further overnight after Bank of Japan politician Kazuo Ueda indicated monetary policy will stay easy as he kept rates unchanged and shown small to no support for the embattled currency during the press conference.

While investors had not expected the BoJ to change its policy this week, there was an results that Ueda would strike a hawkish speech respecting future rate estimates to slow the yen’s decline.

Instead, Ueda said at a news conference on Friday that the central bank’s board members judgesed there was “no major impact” from the weatherer yen on underlying inflation for now.

“Currence rates is not a mark of monetary policy to straight control,” He said.

“But currency flexibility could be an crucial maker in influencing the economy and prices. If the impact on underlying inflation becomes besides large to ignore, it may be a reason to adjust monetary policy.“

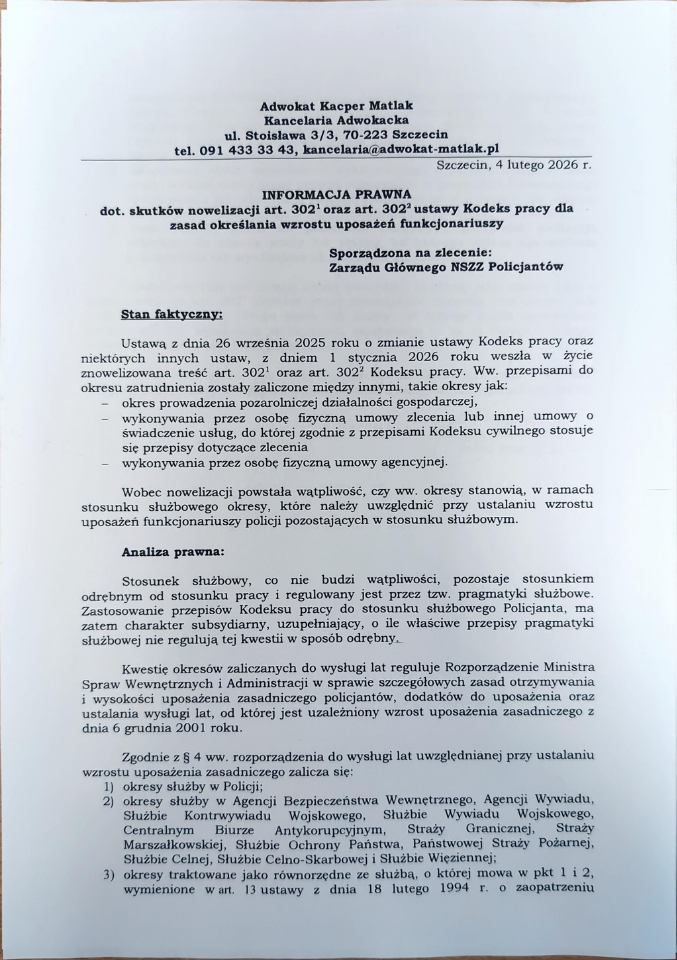

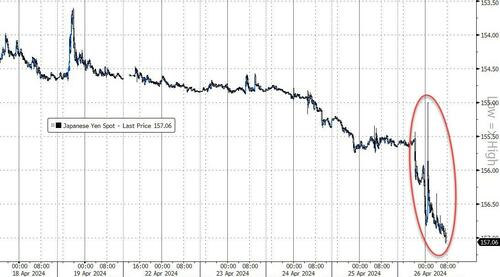

And that sent the currency reeling (amide chaotic swings) back above 157/USD...

Source: Bloomberg

“There is no intention by the BoJ to halt the yen’s decline, at least looking at its message and its outlook report,” said UBS economist Masamichi Adachi.

“The finance minister will gotta act [to stem the yen weatherness]... It would have had been more effective if both the government and the BoJ face the same direction,’ he added.

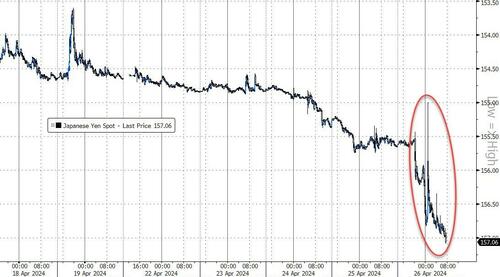

Blowing further below the 'interventionist' levels see erstwhile to a fresh 34-year low...

Source: Bloomberg

“Markets stay on advanced alert for any indication of who the yen’s current weakness will be interpreted as a Lasting inflationary signal,” said Naomi Fink, global strategist at Nikko Asset Management.

“The BoJ nevertheless is likelier to find any knock-on impact from yen weather upon inflation as more concerting than short-term currency moves.”

Driving the depreciation is the yawing gap between the interesting rates in the US – which are at highest in decades after the Fed’s aggressive tighting cycle last year – and these in Japan, where borrowing costs stay stubbornly low close zero.

“Intervention is possible at any time, but it could have been just any selling a large flight, which stalled intervention specification and spurred follow-through moves,” said Koji Fukaya, a Fellow at marketplace hazard Advisory Co. in Tokyo.

“It does not look like intervention, but the only way to confirm is to check data that will be released later by the Ministry of Finance.”

Policymakers have repeatedly damaged that depreciation won’t be tolerated if it goes besides far besides fast.

Finance Minister Shunichi Suzuki reiterated after the BoJ gathering that the government will respond according to abroad exchange moves.

Potential triggers for interventions are public holidays in Japan on Monday and Friday next week, which brings the hazard of flexibility amid thought trading.

“Shoud the yen fall further from here, like after the BOJ decision in September 2022, the anticipation of intervention will increase,” said Said Hirofumi Suzuki, Chiefcurrence strategist at Sumitomo Mitsui Banking Corp.

“It is not the level but it’s the velocity that will trigger the action.”

But so far, nothing! And so the marketplace continues to call Ueda and Suzuki's bluff, knowing full well that a abrupt intervention will possibly briefing support the currency but will pancake the current gains in nipponese stocks.

However, not everyone is convinced intervention is imminent.

In a note this morning, Deutsche Bank says the currency’s decline is guaranteed and finally mark the day where the marketplace has realized that Japan is following a policy of reward request for the year.

We have long argued that FX intervention is not credible and the toning down of verbal jankboning from the finance minister overnight is on balance a affirmative from a credibility perspective. The ability of intervention can’t be routinely out if the marketplace turns differently, but it is besides noted that politician Ueda played down the import of the yen in his press conference present as well as signaling no urgency to hike rates. We would frame the ongoing yen collapse around the following points.

Yen weakness is simply not that bad for Japan. The tourism sector is booming, profit margins on the Nikkei are soaring and exporter competence is increasing. True, the cost of imported items is going up. But growth is fine, the government is helping offset any of the cost via subsidies and core inflation is not accelerating. Most importantly, the nipponese are large abroad asset owners via Japan’s affirmative net global investment position. Yen weakness so leads to large capital gain on abroad bonds and equities, most easy summarized in the reflection that the government pension fund (GPIF) has truly made more profits over the last 2 years than the last 20 years combined.

There simply is simply a problem. Japan’s core CPI is around 2% and has been decelerating in the last months. The Tokyo CPI overnight was 1.7% exclusive one-off effects. To be sure, inflation may well accelerate again helped by FX weather and advanced weight growth. But the starting point of inflation is exclusively different to the post-COVID Hiking cycles of the Fed and ECB. By extension, the inflation pain is far little and the originality to hike far little too. No where is this more environment than the fact that nipponese consumer assurance are close to their cycle highs.

Negative real rates are great. There is simply a large attraction to moving negative real rates for the consolidated government balance sheet. As we demonstrated last year, it created fiscal space via a $20 trillion carry trade while besides generating asset gain for Japan's wealthy voting base. This enthusiasts the persistent home capital outflows we have been highlighting as a key driver of yen weatherness over the last year and that have pushed Japan’s broad basic balance to be 1 of the weeks in the world. It is not speculators that are taking the yen but the nipponese themselves.

The bottom line, Deutscxhe deals, is that for the JPY to turn strongr the nipponese request to unwind their carry trade. But for this to make sense of the Bank of Japan needs to engineer an expedited Hiking cycle akin to the post-COVID experiences of another central banks. Time will tell if the BoJ is moving besides slow and generating a policy mistake. A shift in BoJ inflation forecasts to well above 2% over their forecast horizon would be the clearest signal of a shift in reaction function. But this isn’t happening now.

The nipponese are enjoying the ride.

But there is possible for yen upside as Bloomberg’s Simon White notes that profit taking on abroad asset positions might shortly advance any yen repatriation and force USD/JPY lower.

If it is perceived that the yen won’t get much cheerer due to intervention risk, home investors might choose to start switching any of their US equity positions back to the home market, repatring yen and pressuring USD/JPY lower in the process.

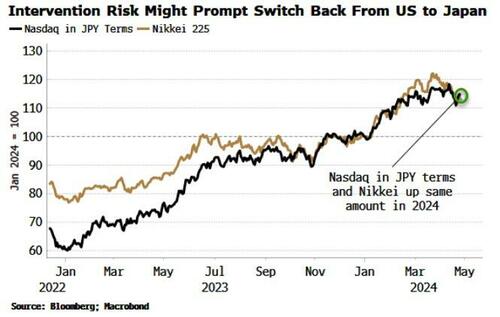

The illustration below shows that on the year, the Nasdaq in yen terms and the Nikkei are both up by the same 13%-14% on the year. A Stronger yen would present an ongoing headwind to the US position.

Equity positions are typically little FX hedged than bond positions, meaning that the repatriation of the currency is not required by the unwind of the hedge.

The dynamics of place trading, options barriers and possible intervention as well as US PCE data released later present will dominate the currency's short-term gyrations, but the lightly longer-term considerations of profit taking on abroad positions will start to drive the medium-term outlook.

Once that trend is established ittself, the hanger-term drivers of the yen will come into focus. Japan is the world’s largest net creditor, and there is simply a crucial structural short in the yen.

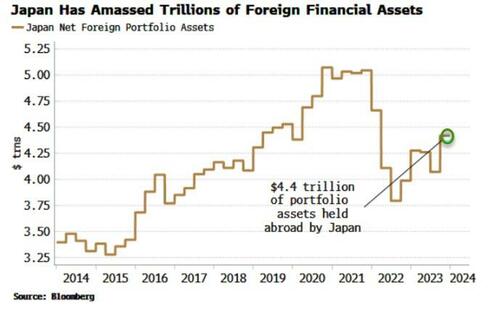

The country’s net global investment position is $3.3 trillion, but its net position in portfolio assets, i.e. so-called hot flows that could be liquidated quickly, is $4.4 trillion.

Only a fraction of that being repatriated has signedant possible to drive the yen considerably higher.

The question is, how much pain is China willing to take from its regional neighbourhood’s 'devalue’?

Tyler Durden

Fri, 04/26/2024 – 10:50