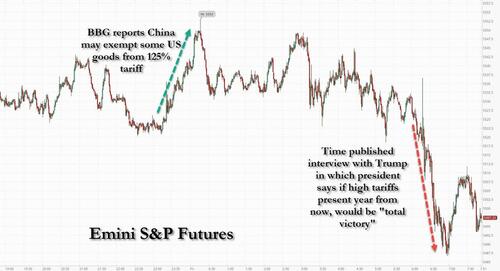

Futures Slide After Trump Interview Reverses Boost From China Tariff Cut Reports

US equity futures are mixed after three days of gain, with tech leading, highlighted by GOOG (+5.6% amid strong earnings results last night), META (+3.5%), and TSLA (+1.6%). S&P futures first rose to session highs during the Asian session, when sentiment was first buoyed by dovish remarks from Fed officials Christopher Waller and Beth Hammack, which bolstered expectations for a potential interest-rate cut as soon as June; but the session highlight was a Bloomberg report that China was considering suspending its 125% tariff on some US imports including plane leases, indicating a shift in the game theoretical „game of chicken” balance and suggesting a deal may come sooner than expected as pain levels are rising for Beijing. Later, foreign ministry spokesman Guo Jiakun reiterated that China is not in talks with the US over tariffs, contradicting Trump and underscoring the complexities for investors tracking headlines out of Washington and Beijing. Futures then slumped to session lows just after 6am ET after Time published an interview with Trump (which took place on April 22) in which the president said China’s President Xi has called him (something China denies), said he would not call XI himself, and when asked if high tariffs are still present a year from now, Trump said that would be a „total victory” adding that he expects trade deals in the next 3-4 weeks. In other words, if China may have been offering an olive branch before the interview, those hopes were dashed after its publication and S&P futures reflected that, sliding to session lows down about 0.4% after earlier they rose by the same amouint.

The dollar strengthened, while the yen and Swiss franc retreated as investor demand for non-US haven assets waned. Gold slid 1.5%. Treasuries extended their gains from Thursday; Bond yields dropped (2-, 5-, 10-yr yields are 0.8bp, -0.2bp, -1.6bp lower). Commodities were mixed with Base Metals higher and Precious Metals lower. The US session includes revised April University of Michigan sentiment gauges, and Fed’s external communications blackout ahead of the May FOMC meeting starts Saturday.

In premarket trading, Alphabet shares jumped as much as 5% after posting first-quarter revenue and profit that exceeded analysts’ expectations, buoyed by continued strength in its search advertising business. Alphabet was the top gainer in the Magnificent Seven stocks (Alphabet +4.9%, Meta +3.2%, Amazon +0.5%, Tesla +0.9%, Nvidia +0.4%, Microsoft -0.2%, Apple -0.8%; Alphabet rises 4.9%). Intel tumbled 7% as CEO Lip-Bu Tan gave investors a stark diagnosis of the chipmaker’s problems, along with the sense that it will take a while to fix them. Gilead drops 3.9% after the biopharmaceutical company posted 1Q revenue that fell short of estimates as sales of Trodelvy and Veklury disappointed. Here are some other notable premarket movers:

- Eastman Chemical Co. (EMN) falls 2.3% after the chemicals and plastics maker provided a disappointing second-quarter profit forecast, citing factors including tariffs between the US and China.

- Hasbro rises 1.0% as Citi upgrades to buy, citing underlying momentum of the toymaker’s business.

- Ironwood Pharmaceuticals climbs 9.3% after the company reaffirmed its revenue forecast for the full year.

- Sphere Entertainment rises 13% after its wholly-owned unit MSG Networks reached a deal to restructure the debt of its subsidiaries and amend the media rights agreements with the New York Knicks and the New York Rangers.

- T-Mobile falls 5.7% after the company reported fewer new wireless phone subscribers than analysts expected in the first quarter.

- Skechers USA slides 6.9% after the footwear company said it’s not providing financial guidance and withdrawing its previous annual outlook due to macroeconomic uncertainty.

On the trade front, Bloomberg News reported that China is considering suspending its 125% tariff on some US imports. Later, Foreign Ministry spokesman Guo Jiakun reiterated that China isn’t in talks with the US over tariffs, contradicting President Donald Trump and underscoring the complexities for investors tracking headlines out of Washington and Beijing.

“We are currently in tariff purgatory,” said Joachim Klement, strategist at Panmure Liberum. “There is no fundamental change to the outlook, so markets latch on to noise and get constantly whipsawed by the ever-changing utterances of Donald Trump and his cabinet.”

Confirming that, in an interview Time published with Trump just after 6am ET, and which took place on April 22, Trump said China’s President Xi has called him even though China has denied this; when asked if high tariffs are still present a

year from now, Trump said that would be a „total victory.”

- In the interview, Trump said tariffs are still necessary.

- „If we still have high tariffs, whether it’s 20% or 30% or 50%, on foreign imports a year from now, will you consider that a victory?”, he responded, „Total victory”

- When asked if he would call Xi (if Xi did not call him), Trump replied „No”.

- US Treasury Secretary Bessent and Secretary of Commerce Lutnick „did not tell me” to do a 90-day pause.

- ”1 certainly don’t mind having a tax increase” on millionaires

- Being serious when talking about acquiring the Panama canal, Greenland, and making Canada the 51st state

- Trade deals expected in the next 3-4 weeks

More recently, on Thursday, Trump said his administration was talking with China, even as Beijing denied the existence of negotiations and demanded the US revoke all unilateral tariffs. Meanwhile, the US and South Korea could reach an “agreement of understanding” on trade as soon as next week, said Treasury Secretary Scott Bessent.

Traders also took some early comfort from hopes that the Fed may reduce interest rates earlier than expected. Markets currently favor a quarter-point cut in June and a total of three such reductions by year-end. Fed Governor Christopher Waller said he’d support rate cuts in the event aggressive tariffs under President Trump’s trade policies hurt the jobs market, speaking on Bloomberg Television. Cleveland Fed President Beth Hammack told CNBC the central bank could move on rates as early as June if it has clear evidence of the economy’s direction.

While the dollar was on course for its first weekly gain in a month, Bank of America strategists said investors should sell into rallies in US stocks and the greenback, cautioning that the conditions for sustained gains are missing. The dollar is in the midst of a longer term depreciation while the shift away from US assets has further to go, according to the BofA team led by Michael Hartnett. The trend would continue until the Fed starts cutting rates, the US reaches a trade deal with China and consumer spending stays resilient. The depreciation of the dollar is the “cleanest investment theme to play,” according to Hartnett.

The Stoxx 600 rises 0.3%, on track for a fourth day of gains as worries about trade tensions between China and the US subsided, with most significant moves triggered by a continued deluge of earnings, including from Saab and Safran. Alten and Hemnet are among the biggest laggers. Here are the biggest movers Friday:

- IMCD shares rise as much as 8.5% after the chemicals maker’s earnings met expectations, which analysts said was a relief given yesterday’s plunge on the shock news its CEO was leaving

- Saab shares gain as much as 4.3%, reversing earlier declines of 5.2%. The Swedish defense firm’s 1Q earnings beat expectations, though their order intake missed

- Safran shares rise as much as 4.8% after the French aerospace and defense firm reported adjusted revenue for the first quarter that beat the average analyst estimate

- Yara shares rise as much as 5.7% after the Norwegian agricultural chemicals firm reported adjusted Ebitda for the first quarter that beat the average analyst estimate

- Accor shares rise as much as 5.6% to the highest level this month. Analysts say the French hotel operator’s results are favorable, noting positive demand commentary and expectations for net unit growth throughout the year

- Saint-Gobain rises as much as 4.3% after the construction materials producer’s 1Q. Analysts are generally positive on the results, with Morgan Stanley praising the firm’s consistent delivery

- Alten shares slide as much as 12% after the French IT firm reported a 5.5% drop in organic sales in 1Q, warning that some of its major clients are freezing or postponing projects due to tariff uncertainties

- Hemnet shares drop as much as 11%, their worst drop since October, after the Swedish property platform missed expectations in the first quarter, giving up gains leading into the results

- Kemira shares fall as much as 15%, the steepest drop in almost 14 years, after the Finnish chemicals company warned over the impact on end-markets of increased economic uncertainty

- Mobico Group shares plunge as much as 11% after the company announced it is selling its school bus business in North America. Analysts said the price tag is disappointing

Asian equities also advanced after a Bloomberg report said Beijing is weighing a suspension of its 125% tariff on some US imports, though the Chinese Foreign Ministry spokesman Guo Jiakun later denied that they’re in talks with the US.

Earlier in the session, Asian stocks gained as signs of progress in trade negotiations boosted sentiment, with a major regional benchmark erasing all losses driven by Trump’s April 2 Liberation Day announcement of reciprocal tariffs. The MSCI Asia Pacific Index rose 0.9%, with TSMC and Tencent among the biggest contributors. Benchmarks in Taiwan, Hong Kong, Japan and South Korea all advanced. The key MSCI Asian index joins benchmarks in India, Korea, Australia and Indonesia in recouping losses from this month’s tariff selloff. The regional gauge is on track to cap its second-straight week of gains. Meanwhile, stocks and bonds tumbled in India, as traders braced for a potential worsening of the geopolitical situation with neighboring Pakistan. Indian shares were the worst performers in Asia on Friday, while the rupee and the nation’s bonds also slid, indicating growing angst among traders over any further ramping up of tensions between the two nuclear-armed nations. Markets are closed in Australia and New Zealand for holidays Friday. Key events to watch next week include rate decisions in Japan and Thailand as well as China PMI data.

In FX, the Bloomberg Dollar Spot Index rose as much as 0.4% and is set to notch its first weekly gain in a month. The greenback gained versus all G-10 currencies; The Japanese yen is among the weakest of the G-10 currencies, falling 0.5% against the greenback; USD/JPY rises 0.8% to 143.85.

In rates, Treasury futures rose to session highs in early US trading, with yields 1bp-4bp richer across a flatter curve, outperforming European bonds after stronger-than-expected UK retail sales data. The 10-year yield near 4.29% was ~3bp richer on the day, outperforming German counterpart by 5bp, UK by 2bp. Among US yield-curve spreads, 2s10s and 5s30s are 1bp-2bp flatter. Shorter-dated maturities also underperform in Germany where two-year borrowing costs rise 4 bps.

In commodities, WTI falls 0.5% to $62.50 a barrel. Bitcoin rises 2% to just shy of $95,000. Haven assets underpeform, with gold falling nearly $50 to below $3,300/oz.

Looking at today’s calendar, the US session includes revised April University of Michigan sentiment gauges, and Fed’s external communications blackout ahead of the May FOMC meeting starts Saturday.

Market Snapshot

- S&P 500 mini -0.2%

- Nasdaq 100 mini -0.3%

- Russell 2000 mini -0.5%

- Stoxx Europe 600 +0.1%

- DAX +0.4%

- CAC 40 +0.7%

- 10-year Treasury yield -3 basis points at 4.28%

- VIX +0.4 points at 27

- Bloomberg Dollar Index +0.3% at 1227.23,

- euro -0.3% at $1.1353

- WTI crude -0.3% at $62.6/barrel

Top Overnight News

- China has exempted some U.S. imports from its 125% tariffs and is asking firms to identify critical goods they need levy-free, according to businesses notified, in the clearest sign yet of Beijing’s concerns about the trade war’s economic fallout. RTRS

- Apple plans to import most of the iPhones it sells in the US from India by the end of next year, accelerating a shift beyond China, people familiar said. The goal will require Apple to double its India capacity. BBG

- President Trump signed an executive order boosting the deep-sea mining industry, while the order instructs the Commerce Secretary to expedite permits under the Deep Seabed Hard Mineral Resource Act, as well as instructs the Commerce and Interior Departments to issue a report on opportunities for seabed mineral exploration on the US outer continental shelf.

- China aims to implement more growth-supporting measures amid rising challenges from hefty U.S. tariffs. The government will seek to coordinate policy measures to support domestic economic aims amid external economic and trade struggles. the government intends to cut interest rates and the amount of cash banks are required to set aside at the central bank, while making full and effective use of existing fiscal and monetary policies, the Politburo said. WSJ

- Bessent says South Korea trade negotiations are moving along at a faster pace than anticipated. Nikkei

- US Republicans in Congress are to unveil a $150bln defense spending package including $27bln for Trump’s Golden Dome missile defense and $29bln for shipbuilding.

- Japan is considering a proposal that would see it boost purchases of US soybeans to compensate for a drop in China demand. Nikkei

- Tokyo inflation picked up to 3.4% in April, its fastest in two years and supporting the BOJ’s rate-hike stance. BBG

- A US-India trade agreement under discussion will cover 19 categories, including greater market access for farm goods, e-commerce, data storage and critical minerals, people familiar with the matter said, the first step toward a deal that may help the South Asian nation evade higher tariffs on its goods. BBG

- UK retail sales unexpectedly rose for a third straight month in March, helped by record-breaking sunshine. But GfK data showed consumer confidence slid to the weakest level in 17 months in April. BBG

- Russia’s oil producers are drilling at the fastest pace in at least five years, preparing for potential OPEC+ output hikes and possible sanction relief. Activity is more than a third above pre-war levels. BBG

- Fed’s Kashkari (2026 voter) said a resolution of trade frictions would relieve uncertainty and would be optimistic, while he is worried that businesses will resort to layoffs amid uncertainties and noted some businesses say they are scenario planning for potential layoffs if uncertainty lasts although he is not seeing an uptick in layoffs yet. Furthermore, Kashkari said the frequency of announcements out of Washington has created a challenge for policymakers and for everybody.

Trade/Tariffs

- China held a meeting on responding to trade frictions, according to the Commerce Ministry; said Trade frictions enter a high-intensity phase and are facing difficulties and challenges China said to stay confident in handling trade tension; adopt strategic approaches. To focus on preventing and resolving trade risks. Trade frictions enter a high-intensity phase and are facing difficulties and challenges. Cultivate new opportunities in crisis.

- China’s Foreign Ministry said it is not having any consultations or negotiations with the US on tariffs; on tariff exemptions, said not familiar with specifics

- China is said to consider exempting some US goods from tariffs as costs increase with Chinese authorities considering removing additional levies for medical equipment and some industrial chemicals like ethane, according to Bloomberg citing sources familiar with the matter. It was also reported that several Chinese tech companies confirmed that eight tariff codes related to semiconductors and integrated circuits are now exempt from additional tariffs, according to Caijing.

- US Treasury Secretary Bessent said he had a good meeting with South Korea and they are moving faster than thought, while they will talk technical terms and could get to terms next week.

- South Korea’s Trade Minister said South Korea and the US agreed in principle on the framework for trade talks. It was also reported that South Korea’s Finance Minister said they will try their best to produce meaningful results by July 8th and that autos were in focus during talks, while the two countries reached common ground on discussing measures on tariffs and non-tariff barriers, economic security, investment cooperation, and currency policy. Furthermore, technical-level talks between South Korea and the US will be held in Seoul on May 15th-16th and South Korea’s Industry Minister said they reached a common ground on shipbuilding cooperation with the US.

- Japanese Finance Minister Kato met US Treasury Secretary Bessent and told him that US tariffs are deeply regretful, while they agreed the FX rate should be set by markets and that excessive volatility has an adverse effect on the economy. It was also reported that Japan is weighing buying more US soybeans as part of a tariff deal and is also considering boosting US corn imports.

- Canadian Finance Minister Champagne said they need to fight against the US tariffs, which are still affecting a large portion of Canadian goods. Furthermore, he said the scheduling was too tight for a bilateral meeting with US Treasury Secretary Bessent but they did interact at the G7 meeting in Washington.

- US reportedly seeks India trade deal on e-commerce, crops, and data storage, according to Bloomberg sources.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly gained as the region took impetus from the rally on Wall St amid trade-related optimism after President Trump suggested that the US and China held talks despite a denial by the latter. However, conditions were somewhat quieter for most of the session with the absence of markets in Australia and New Zealand for a holiday, although there was a slight boost on reports that China is said to consider exempting some US goods from tariffs. Nikkei 225 rallied at the open but with further gains initially capped as participants digested firmer-than-expected Tokyo CPI before the China tariff story provided a late tailwind. Hang Seng and Shanghai Comp were somewhat varied as the Hong Kong benchmark rallied amid strength in property, tech and casino stocks, while the mainland lagged following the conflicting statements by the US and China on whether trade talks took place.

Top Asian News

- China’s Politburo said China’s fiscal policy will be more proactive, economic recovery needs to be further reinforced; China to cut RRR and rates when needed and in a timely manner; Vows to fully prepare emergency plans for external shocks. Use well moderately loose monetary policy China to cut RRR and rates when needed and in a timely manner. To create new structural monetary tools Vows to fully prepare emergency plans for external shocks. Improve policy toolbox for stabilising employment and the economy. Implement established policies early. Will speed up issuance of ultra-long bonds.

- PBoC Governor Pan affirmed monetary policy is to be moderately loose and said they will defend global economic stability, while he vowed to drive the Chinese economy and said China’s economy is off to a good start, continues to rebound positively, and the financial market is running smoothly.

- China’s Finance Minister attended the G20 meeting in Washington and said the current world economic growth momentum is insufficient and tariff wars and trade wars have further affected economic and financial stability.

- Japanese PM Ishiba said he decided on a package of measures to deal with US tariffs and instructed cabinet members to do the utmost to aid small and medium-sized enterprises that will be affected.

- Donald Trump Jr is to meet South Korean business leaders on April 30th, according to Yonhap.

- PCA sees China’s April car sales up 14.4% to 1.75mln Units, via Bloomberg

European bourses (STOXX 600 +0.4%) opened entirely in the green with sentiment boosted by positive trade updates from China, and following a stellar Alphabet earnings report. However, around the time of the European cash open, sentiment waned a touch – but this ultimately proved fleeting. European sectors opened with a strong positive bias but is a little more mixed now. Travel & Leisure takes the top spot, with the sector propped up by post-earning strength in Accor (+4%) and Evoke (+1%). The former topped Q1 revenue expectations and highlighted that it saw “no cracks in demand” so far (re. hotels).

Top European News

- SNB Chairman Schlegel said the main instrument is interest rate, but forex interventions can also be used to influence monetary conditions. Trade policy situation is creating high uncertainty for all countries, including Switzerland; could fragment the global economy Economic slowdown in Switzerland cannot be ruled out. Price stability cannot prevent trade policy-related uncertainty, but remains very important.

- UK will reportedly be expected to pay a fee to guarantee UK companies access to a EUR 150bln EU weapons fund, according to the FT citing diplomats.

FX

- DXY is nursing some of its recent losses after retreating amid the broad risk-on sentiment on Wall St. Price action during the European morning has been rather contained, with the index in a 99.43-99.89 range at the time of writing. Sentiment today has been boosted by reports that China is considering exempting some US goods from tariffs as costs increase.

- EUR gave back some of the prior day’s gains after hitting resistance just shy of the 1.1400 handle as the greenback regained composure. EUR/USD resides in a 1.1315-1.1394 intraday range.

- JPY breached the 143.00 level to the upside which was facilitated by a rebound in the dollar and the positive risk appetite, while there were also some suggestions of Gotobi demand, whilst a flight out of safe-havens were seen on reports that China is said to consider exempting some US goods from tariffs as costs increase. Tokyo CPI data saw an acceleration, but failed to lift the JPY.

- GBP faded some of Thursday’s advances and eventually gave up the 1.3300 status as the Dollar picked up. Little reaction was also seen this morning to the substantial beat in UK Retail Sales, which was stronger-than-expected. On the trade front, UK Chancellor Reeves said she understands US concerns on trade imbalances, especially in China and they don’t always agree with the US on policy prescriptions but is confident a trade deal can be done.

- Antipodeans are both subdued amid the upticks in the Dollar and overall cautious risk tone amid the uncertain trade environment, whilst markets were closed on both sides of the Tasman for ANZAC Day.

- PBoC set USD/CNY mid-point at 7.2066 vs exp. 7.2898 (Prev. 7.2098).

Fixed Income

- USTs are flat in what has been a rangebound morning thus far as traders digest the latest Bloomberg reports on China, which suggest China is said to consider exempting some US goods from tariffs as costs increase. UST futures rate in a narrow 111.02+ to 111.09 range at the time of writing; docket ahead is thin.

- German debt is taking a breather after steadily climbing to just shy of the 132.00 level, whilst a slew of ECB commentary failed to trigger much price action. In terms of a recent ECB commentary on tariffs, ECB rhetoric leans towards an initial disinflationary narrative around tariffs, with Lagarde calling them a negative demand shock and noting the net inflation impact remains unclear. Knot flagged that a 25% US tariff could shave 0.3ppts off EZ growth.

- Gilts are conforming to price action across peers despite little notable move seen from the above-forecast UK retail sales metrics. On the trade front, UK Chancellor Reeves said she understands US concerns on trade imbalances, especially in China and they don’t always agree with the US on policy prescriptions but is confident a trade deal can be done. Gilt Jun’24 futures currently reside around the middle of a 92.90-93.14 range.

Commodities

- The crude complex has been choppy, trading on either side of the unchanged mark. Early morning sentiment was boosted by reports that China is to consider exempting some US goods from tariffs as costs increase. Around the European cash open, some modest pressure was seen in the complex, but the downside has since stabilised. Brent’Jun 25 currently trading within a USD 66.48-67.11/bbl range.

- Precious metals hold a negative bias, with losses in spot gold more pronounced vs peers, due to the positive risk tone and relatively stronger Dollar. XAU currently towards the lower end of a USD 3,287.16-3,370.79/oz range.

- Base metals are entirely in the red, with losses driven by the relatively stronger Dollar and potentially due to the conflicting commentary of US-China trade talks. 3M LME Copper currently trading in a USD 9,359.5-9,458.8/t range.

- UK’s Unite said TotalEnergies (TTE FP) workers balloted for strike action and that around 50 Unite members based on the Elgin Franklin and North Alwyn platforms are involved.

- Iranian oil minister said Tehran will sign USD 4bln agreement with Russian companies to develop seven oil fields, via state TV.

- ExxonMobil (XOM) reports flaring event at Joliet, Illinois refinery (275k BPD).

Geopolitics: Middle East

- „Haaretz citing sources: No significant progress in the negotiations of the exchange deal between Hamas and Israel so far”, according to Al Jazeera

- China, Russia, and Iran IAEA representatives met with the IAEA Director General on Thursday and had in-depth communication on how the IAEA can play its role in serving the political and diplomatic settlement process of the Iranian nuclear issue.

- US is poised to offer Saudi Arabia an over USD 100bln arms package during President Trump’s visit to the kingdom in May.

Geopolitics: Ukraine

- Russian Foreign Minister Lavrov said the US and Russia are moving in the right direction towards the deal.

- NATO Secretary General Rutte said he had a good meeting with US President Trump and discussed Ukraine, while he does not know if Russian President Putin wants peace but added that something is on the table for Russia-Ukraine and the ball is in Russia’s court. Furthermore, Rutte said it is not accurate that the US pressured Ukraine to accept a deal that favours Russia.

Geopolitics: Other

- „AFP quotes Pakistani official: overnight exchange of fire on border with India”, via Sky News Arabia.

US Event Calendar

- 10:00 am: Apr F U. of Mich. Sentiment, est. 50.5, prior 50.8

DB’s Jim Reid concludes the overnight wrap

Back from Luxembourg and last night stayed up late to watch the final episode of the latest series of „The White Lotus”, one of the most famous dramas of the last few years. If you ever think your life is going through a tough patch please watch this program as many of these guys have some serious issues!!!

At times the series was so uncomfortable that it was a relief to get back to markets and to trade wars. However for now markets continue to recover with US assets in particular catching up on lost performance after the recent normalisation of policy from the US administration. My view is that the damage to US exceptionalism will be longer lasting but that it’s understandable that there’ll be a relief recovery after the US has come back from the brink policy wise. It’s also worth noting that before Liberation Day the Mag-7 were notably underperforming, especially since DeepSeek’s arrival onto the scene and a generally disappointing Q4 earnings season for the group. See my CoTD from yesterday here for more on this. How the Mag-7 perform from here will dictate a lot of the US exceptionalism trade.

We had the latest taste of this with Alphabet’s earnings yesterday evening. Google’s parent delivered a decent revenue and earnings beat, mostly driven by its search advertising business, and announced a 5% dividend increase. Its shares rose by close to 5% in post-market trading, following on a +2.37% gain in the regular session. S&P 500 (+0.51%) and NASDAQ 100 (+0.62%) futures are trading higher overnight helped by these results. Next stop for the Mag-7 will be the releases from Microsoft, Meta, Amazon and Apple on Wednesday and Thursday next week. So a big couple of days ahead next week. Interestingly the FT have just broken a story as we go to print saying that Apple plans to shift the assembly of all US-sold iPhones to India as soon as next year. This is a big move away from China and shows how the geopolitics are shifting. It’s a big win for India.

As trade and geopolitics are reshaping, for now investors are becoming more relaxed about the near-term outlook with few signs of deteriorating data as yet and some dovish comments from Fed officials yesterday, which reassured investors that the Fed would still cut rates if the labour market deteriorated. So collectively, that helped the S&P 500 (+2.03%) to post a third consecutive gain for the first time since Liberation Day. And in another sign that market stress was easing, the VIX index (-1.98pts) fell to its lowest since the April 2 tariff announcements, closing at 26.47pts.

Those comments from Fed officials really helped to support the market yesterday, as they were notably more dovish than Chair Powell, who’d sounded a lot more concerned about inflation. For instance, Fed Governor Waller repeated his previous view that tariffs just represented a one-time price effect, and said that if he saw “a significant drop in the labor market, then the employment side of the mandate, I think, is important that we step in.” Earlier, we also heard from Cleveland Fed President Hammack, who said that if they had “clear and convincing data by June, then I think you’ll see the committee move if we know which way is the right way to move at that point in time”. So that was seen as opening the possibility of a rate cut sooner than expected, and futures moved to price in 85bps of cuts by the December meeting, up +6.0bps on the day. And in turn, Treasuries saw a strong rally, with the 10yr yield (-6.7bps) falling back to 4.32%, marking its third consecutive decline.

Aside from those remarks, the other good news yesterday was that the labour market appeared to remain in decent shape for the time being. For instance, the weekly initial jobless claims were at 222k over the week ending April 19, in line with expectations. Moreover, that was completely in line with where they’ve been over recent weeks, having oscillated between 216k-225k for the last 8 consecutive weeks now. So yet again, there was no obvious sign that layoffs were increasing, and we even saw continuing claims (for the week ending April 12) fall back to 1.841m (vs. 1.869m expected), which was their lowest since late-January.

All that helped to spur a strong market rally, with most US assets continuing to unwind their post-Liberation Day moves. For instance, the S&P 500 (+2.03%) posted a third consecutive gain, and it was actually the first time since February 2023 that the index has managed three consecutive gains of more than +1% a day. Tech stocks led the advance, with the Magnificent 7 (+2.94%) now up by +9.67% over the last three sessions.

When it came to the latest on tariffs, the most notable headline was Trump suggesting that his administration has been talking with China on trade. This came in contrast to comments from China officials earlier in the day, who said that there were no trade negotiations currently happening and that the US should revoke its unilateral tariffs if they wanted to start trade talks. Overnight Bloomberg are reporting that China is considering carving out exemptions to its tariffs on US goods given the stress it’s causing in some areas. So whatever officials say there seems to be movement on both sides to pull back from the most extreme position of the last few weeks.

In terms of other trade talks, Treasury Secretary Bessent said that the US and South Korea could reach an “agreement of understanding” as soon as next week. This followed similar comments earlier in the week on progress in talks with India and added to the sense that the US is keen to announce some agreements soon, even if these represent only rough outlines of the eventual deals.

Back in Europe, markets also put in a decent performance for the most part, which was similarly supported by more robust data than expected. In particular, the Ifo’s business climate indicator from Germany unexpectedly rose to a 9-month high of 86.9 in April (vs. 85.2 expected). Fiscal expansion plans must be helping. Moreover, the expectations component only saw a modest pullback to 87.4 (vs. 85.0 expected), thus avoiding the sharp drop that was widely expected.

That backdrop helped to support European assets across the board, with the STOXX 600 (+0.36%) posting a modest gain by the close. It also meant that the index is now up just over 10% from its low on April 9, just before Trump announced the 90-day tariff extension. In the meantime, sovereign bonds also put in a strong performance, with yields on 10yr bunds (-5.0bps), OATs (-7.2bps) and BTPs (-8.4bps) all coming down. And that got further support from ECB officials, particularly as Olli Rehn said that they shouldn’t rule out a larger cut, and chief economist Philip Lane said “there’s no reason to say we’re always going to do the default 25”.

In Asia, Japanese markets are the best performers with the Nikkei (+1.83%) and the Topix (+1.37%) trading sharply higher after the Japanese government unveiled a package of emergency measures to counter the impact of tariffs. Elsewhere, the Hang Seng (+1.36%) and KOSPI (+1.02%) are performing well. Mainland Chinese stocks are a little more subdued with the CSI (+0.30%) and the Shanghai Composite (+0.15%) only a touch higher. Even with the Apple news mentioned above, Indian stocks (-0.90%) are lower as tensions are very elevated with Pakistan at the moment around Kashmir. Meanwhile, Australian markets are closed for a holiday.

Early morning data showed that Tokyo CPI grew more than expected, rising to a two-year high of +3.5% y/y in April (v/s +3.3% expected) amid a recovery in private spending. It followed a +2.9% increase the prior month. Core CPI rose +3.4% y/y in April (v/s +3.2% expected) after advancing +2.4% the previous month thus increasing speculation over more interest rate hikes by the BOJ.

To the day ahead now, and US data releases include the University of Michigan’s final consumer sentiment index for April. Elsewhere, we’ll get UK retail sales for March. Otherwise, central bank speakers include the BoE’s Greene.

Tyler Durden

Fri, 04/25/2025 – 08:29